Long-term assets are also described as noncurrent assets since they are not expected to turn to cash within one year of the balance sheet date.

The long-term assets are usually presented in the following balance sheet categories:

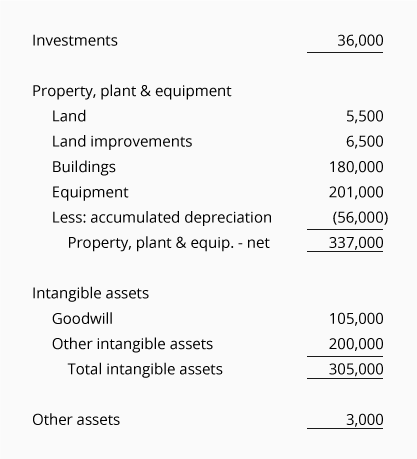

Here is the long-term (or noncurrent) asset section from our sample balance sheets:

The first long-term asset Investments will include amounts such as the following:

While long-term investments in marketable securities are initially recorded at their cost, the amount of these investments will be adjusted (increased or decreased) to report their market value as of the date of the balance sheet.

The balance sheet category property, plant and equipment – net includes the cost of the noncurrent, tangible assets that are used in a business minus the related accumulated depreciation. (These assets are sometimes referred to as fixed assets, plant assets, long-lived assets, and capital assets.)

An asset’s cost minus its accumulated depreciation is known as the asset’s book value or carrying value.

NOTE: The depreciation and the accumulated depreciation reported on a company’s financial statements are typically based on the assets’ years of useful life.

These amounts are likely different from the amounts reported on the company’s income tax return.

The following amounts often appear under property, plant and equipment – net or will be disclosed in the notes to the financial statements:

Land refers to the land used in the business, such as the land on which the production facilities, warehouses, and office buildings were (or will be) constructed. The cost of the land is recorded and reported separately from the cost of buildings since the cost of the land is not depreciated.

Land improvements include parking lots, lighting, driveways, etc. These will be depreciated over their useful lives.

The line buildings and improvements reports the cost of the buildings and improvements but not the cost of the land on which they were constructed. For financial statement purposes, the cost of buildings and improvements will be depreciated over their useful lives.

The cost of a company’s production assets is reported on the balance sheet as equipment or as machinery and equipment. Since the machinery and equipment will not last forever, their cost is depreciated on the financial statements over their useful lives.

Furniture and fixtures reports the cost of these items. Their cost will be depreciated on the financial statements over their useful lives.

The long-term asset construction in progress accumulates a company’s costs of constructing new buildings, additions, equipment, etc. Each project’s costs are accumulated separately and will be transferred to the appropriate property, plant, or equipment account when the asset is placed into service. At that point, the depreciation of the constructed asset will begin.

Accumulated depreciation reports the cumulative amount of depreciation that was recorded on the financial statements since the time that the depreciable assets were purchased and put into service. (The cost of land and the costs reported as construction in progress are not depreciated.)

The general ledger account Accumulated Depreciation will have a credit balance that grows larger when the current period’s depreciation is recorded. As the credit balance increases, the book (or carrying) value of these assets decreases.

You can learn more about depreciation expense and accumulated depreciation by visiting our topic Depreciation.

Intangible assets are described as assets without physical substance. The intangible assets that were purchased (as opposed to the result of effective advertising, training, etc.) are reported on two long-term asset lines:

Goodwill is an intangible asset that is recorded when a company buys another business for an amount that is greater than the fair value of the identifiable assets. To illustrate, assume that a corporation pays $5 million to acquire a business that has tangible and identifiable intangible assets having a fair value of $4 million. The $1 million difference is recorded as the intangible asset goodwill.

Goodwill is assumed to have an indefinite useful life. Therefore, the recorded amount of goodwill is not amortized to expense. Instead, each year the recorded cost of the goodwill must be tested to see if the cost must be reduced by what is known as an impairment loss.

The line other intangible assets refers to intangible assets other than goodwill that were purchased from another party. Some examples include the following:

Except for trademarks, the amount paid to purchase any of these other intangible assets must be amortized to expense over the shorter of their expected useful life or their legal life.

The noncurrent balance sheet item other assets reports the company’s deferred costs which will be charged to expense more than a year after the balance sheet date.

Please let us know how we can improve this explanation

Submit Feedback No ThanksA restricted asset for the purpose of retiring a bond.

Investments in common stock, preferred stock, corporate bonds, or government bonds that can be readily sold on a stock or bond exchange. These investments are reported as a current asset if the investor’s intention is to sell the securities within one year.

The amount of a long-term asset’s cost that has been allocated to Depreciation Expense since the time that the asset was acquired. Accumulated Depreciation is a long-term contra asset account (an asset account with a credit balance) that is reported on the balance sheet under the heading Property, Plant, and Equipment.

This is the period of time that it will be economically feasible to use an asset. Useful life is used in computing depreciation on an asset, instead of using the physical life. For example, a computer might physically last for 100 years; however, the computer might be useful for only three years due to technology enhancements that are occurring. As a consequence, for financial statement purposes the computer will be depreciated over three years.

A cost that has been recorded in the accounting records and reported on the balance sheet as an asset until matched with revenues on the income statement in a later accounting period.